The trading on Wall Street is expected to open today with stability, that is reflected in futures contracts on leading stock indices.

The trading on Wall Street is expected to open today with stability, that is reflected in futures contracts on leading stock indices.

From the final growth figures in France for the fourth quarter of 2016, indicated that the country’s economy grew by 0.4% compared to the third quarter.

Overall, the French economy grew in 2016 by 1.1%, depending on the initial assessment.

The European markets opened today (Tuesday) the trading day on a positive trend at the background of rising prices that have signed yesterday the trading on Wall Street.

The trading on the stock exchanges of Wall Street yesterday ended with a slight rising prices.

The Dow Jones ended at the height of the 12th day in a row, the longest sequence since 1987.

The index rose by 0.1%, as did the S&P 500, and the Nasdaq rose by 0.3%.

The Asian stock markets trading takes place this morning is rising towards the end of a positive month as a result of the increase in indices on Wall Street.

Investors await for the speech by the US president, Donald Trump, in the US Congress tonight.

Trump is expected to provide more details about his economic policies and tax reforms that he wants to lead.

In Japan posted disappointing data indicated a decline in industrial output for the first six months.

The decline was caused by a slowdown in vehicle production

Commodities market this morning:

The WTI oil rising by 0.3% to $ 54.2 per barrel, the Brent oil rising by 0.3% to $ 56.1 per barrel.

The increases are recorded in light of estimates in the market that the demand for commodities going to stabilize the energy market.

Trading Opportunity:

AUD/USD

On a weekly chart the pair stops around a resistance area, as part of a range after a big downtrend.

An opportunity to join in with the line of thought of continued declines can be from the levels of 0.7700 – 0.7650, the trade will be for a longer time frame.

This week, the US president, Donald Trump, will give his first speech at the US Congress, and investors will be alert ahead of the president’s detail regarding economic plans.

Also this week, the chairman of the US Federal Reserve, Janet Yellen, is expected to meet with Chairman of the Mexican equivalent and the International Monetary Fund, and on Friday Yellen expected to give a speech and may provide additional information regarding the feasibility of the Open Market Committee of the Federal Reserve (FOMC) and if will raise interest rates at its next meeting to be held on 14-15 March

Last week summary on Wall Street:

The Dow Jones Industrial Average climbed by 1% on his way to a third straight weekly increases.

The S&P 500 climbed by 0.7%, the fifth consecutive week of gains.

The Nasdaq Composite Index rose by 0.1%, the fifth straight positive week as well.

This morning, the British pound falls by 0.4% against the US dollar to -1.2413 pounds to the dollar at the background of the possibility of a referendum on Scottish independence and separation from the United Kingdom

The WTI oil rising by 0.8% to $ 55.4 per barrel and Brent oil rises by 1% to $ 56.5 per barrel.

Trading Opportunity:

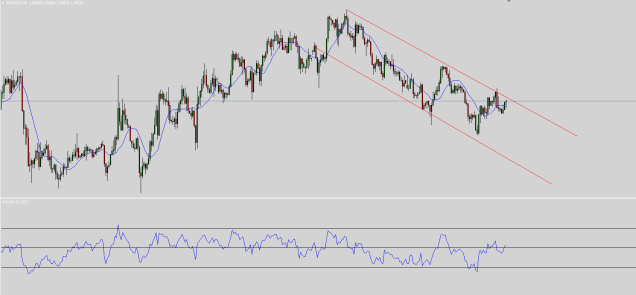

EUR/USD

On 4 hours chart, the pair is going inside a decreasing canal.

The nearest resistance levels are between 1.0600 – 1.0585, from there we can try and look for an entry with the down trend.

The trading on the exchanges of Wall Street ended yesterday with a mixed trend and the Dow Jones continued his longest sequence run in 30 years, after the US finance minister estimated that the US approval of the tax reform will be completed

by the summer.

The energy stocks rose after the oil climbed to a record high of 19 months.

The oil prices closed at the height of the 97 months following an expected moderate increase in US crude stocks.

The price of the gold prices jumped to a three months high after the weakening of the US dollar has increased the demand for the metal as an alternative investment.

France released an economic data on consumer confidence, and it increased to a peak of more than nine years.

The increase in consumer confidence in France in February recorded a rise for the second consecutive month, despite there is uncertainty in the country surrounding the presidential elections to be held in April (first round) and May (second round).

The European stock exchanges trading which takes place this morning is traded with declines as the earnings season continuing.

Trading Opportunity:

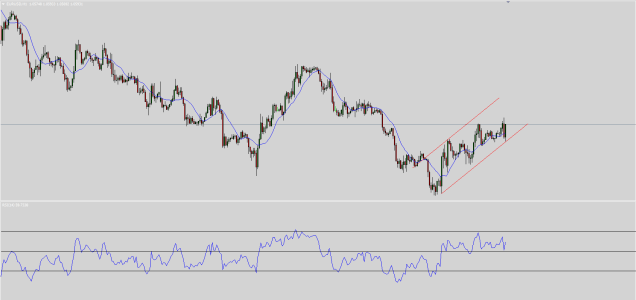

EUR/USD

On an hour chart, after a down trend, it seems that the pair is changing direction on his way up, as when a rising channel was created.

The entry levels to join in with the channel are 1.0575 – 1.0600.

The trading on Wall Street ended yesterday with stability at the backdrop of oil prices fall, and the publication of the protocol of the last meeting of the Fed’s interest, while in Europe the trend was positive.

The protocol of the Fed indicates that overall the members of the Conference of the open market value rate would rise soon as there is uncertainty around the economic policy of the White House.

In fact the protocol of the Fed reflect more confusion than certainty, and the fact that Trump confusing the economists Open Market Committee doesn’t make good effect on the markets and the real economy.

Positive data on existing home sales for January in the United States, these were 5.69 million versus expectations to 5.57 million and 5.49 million existing homes sold last month.

Europe reporting season is in full swing, and investors looking to companies that advertise their financial statements.

Barclays, Glencore, Centrica and Telefonica among others are expected to report later in the day.

Trading Opportunity

USD/CHF

On 4 hour chart the latest main trend is an up trend.

There is a diagonal line which support the rise, also, last week there was a false break which strengthened the trend.

The next opportunity to join in with the next rising wave will be when the price will be around the levels of 1.0080 – 1.0100.

The trading on the stock exchanges of Wall Street yesterday ended with rising prices.

The three major indexes posted new records, as when the Dow Jones rose by 0.6%, capping an eighth consecutive day of gains.

The S&P 500 rose by a similar amount and the Nasdaq added 0.5% to its value.

The recently released economic data, especially the inflation and the manufacturing data, are supporting the positive sentiment in the markets and contributed to the strengthening of the US dollar.

The reporting season is in the final stretch yesterday the retail giant Wal-Mart reported on a net profit of 1.3 dollars per share for its fourth fiscal quarter, one cent above market forecasts.

Revenues totaled about $ 130 billion, compared with analysts’ forecasts which stood at $ 131 billion.

Commodity market,

The price of WTI crude oil rose yesterday by 1.1% to a price level of 54.33 dollars per barrel.

The price of the gold closed with a slight drop of 0.1% (20 cents) and was set on a price level of 1.238.90 dollars per ounce.

Trading Opportunity:

GBP/USD

On an hour chart there is a triangle pattern.

Our main tendency is to look for a brake down of the triangle because it will be a continuity of the previews move of th pair.

If so, the break level will be below 1.2400.

If the pair will break-up the triangle, the entry point will be above 1.2500.

The Asian stock markets trading is conducted today with rising prices, after yesterday there was no trading on Wall Street due to the “Presidents Day”.

The European indexes yesterday closed unchanged, except for the German DAX index which rose by 0.6%.

Good economic news from French, as when the local economy grows fastest since 2011 as services strengthen.

A composite purchasing managers’ Index climbed to 56.2 from 54.1 in January.

In the UK, HSBC shares slide after 62% profit fall.

HSBC attributed the fall to a string of one-off charges, including the sale of its operations in Brazil.

HSBC said its performance had been “broadly satisfactory” given “volatile financial conditions” but warned a rise in global protectionism was a concern.

The bank also announced a smaller-than-expected share buyback.

That also helped undermine shares, which were down by 5% in London.

Among global investors there are feared that the statistical office of President Donald Trump economic data going to be modified.

Trump has not appointed yet anyone from the Council of Economic Advisers in the White House.

The fears of manipulation of the data also arise from the unusual approach of Trump administration’s interpretation of economic data.

The president himself is talking about “real” unemployment much higher than the official, and uses data which cover all citizens of working age who are not employed.

There will be no trading day on Wall Street in honor of the PRESIDENTS DAY.

Investors are waiting to see what is the direction of President Donald Trump regarding his economic policy as well as the tax returns policy.